It’s always exciting, starting an online business — but there are a few important decisions to make before you get going. One of the first is choosing the right business structure: should you register as a sole trader, or a limited company? Or another business model entirely?

The choice you make can affect how you pay tax, how your personal finances are protected, and how you manage your business as it grows. In this guide, we’ll explain the main UK business structures in simple terms and help you decide which option could work best for your situation.

Key takeaways

☑︎ Most online businesses start as sole traders. It’s simple, low-commitment, and easy to change later.

☑︎ The tax picture changes as you earn more. Past around £30,000–£50,000 in profit, a limited company often means paying less.

☑︎ A limited company protects your personal finances. If things go wrong, your savings and assets aren’t on the line.

☑︎ The right structure depends on your income, your risk appetite, and your ambitions.

☑︎ Customers care about how your business looks online. A matching domain name and email address go a long way. You can get it all with 123 Reg hosting plans.

Before you start an online business

Starting a business involves more than just having an idea.

Before you decide whether to register as a sole trader or a limited company, there are a few practical things worth sorting out first. Getting these basics right early on will give your business a much stronger foundation to grow from.

1. Pick a business name

Your business name is one of the first things you’ll need to think about. It should reflect what you do, be easy for customers to remember, and give you room to grow as your business develops.

It’s also worth checking that your chosen name is available and that you can use it consistently across your website, email address and social media profiles. A name that works well online can help customers find and recognise your brand.

2. Get your business online

You don’t need everything else in place before getting your business online. In fact, it’s often a smart move to secure your domain name and professional email address early, even while you’re still figuring out how the rest of the business will take shape.

A domain that matches your business name helps you build a consistent identity from day one, while a professional email address gives customers a simple way to reach you and makes your business look established.

If you’re not sure where to start, check out our AI Domain Search for ideas. It can be a smart move to find the domain first and base the business name on that!

See also: .com vs .co.uk – Which Domain is Best for Your British Business?

3. Register your business

“Do I need to register my online business?” It’s one of the first questions many new business starters ask.

The short answer is: not just to get your website up and running, but yes, once you actually start trading.

So there’s no need to hold off on building your site while you sort out the legal side. You can get online first and take care of registration when you’re ready to open your (virtual) doors. But you will need to register eventually.

If you’re going to trade as a sole trader, you need to register with HMRC for Self Assessment, usually by 5th October in the second tax year of your business. Limited companies register with Companies House before they start trading, which is a simple online process that and often done in less than 24 hours.

Either way, getting registered at the right time helps you stay on top of your responsibilities from day one.

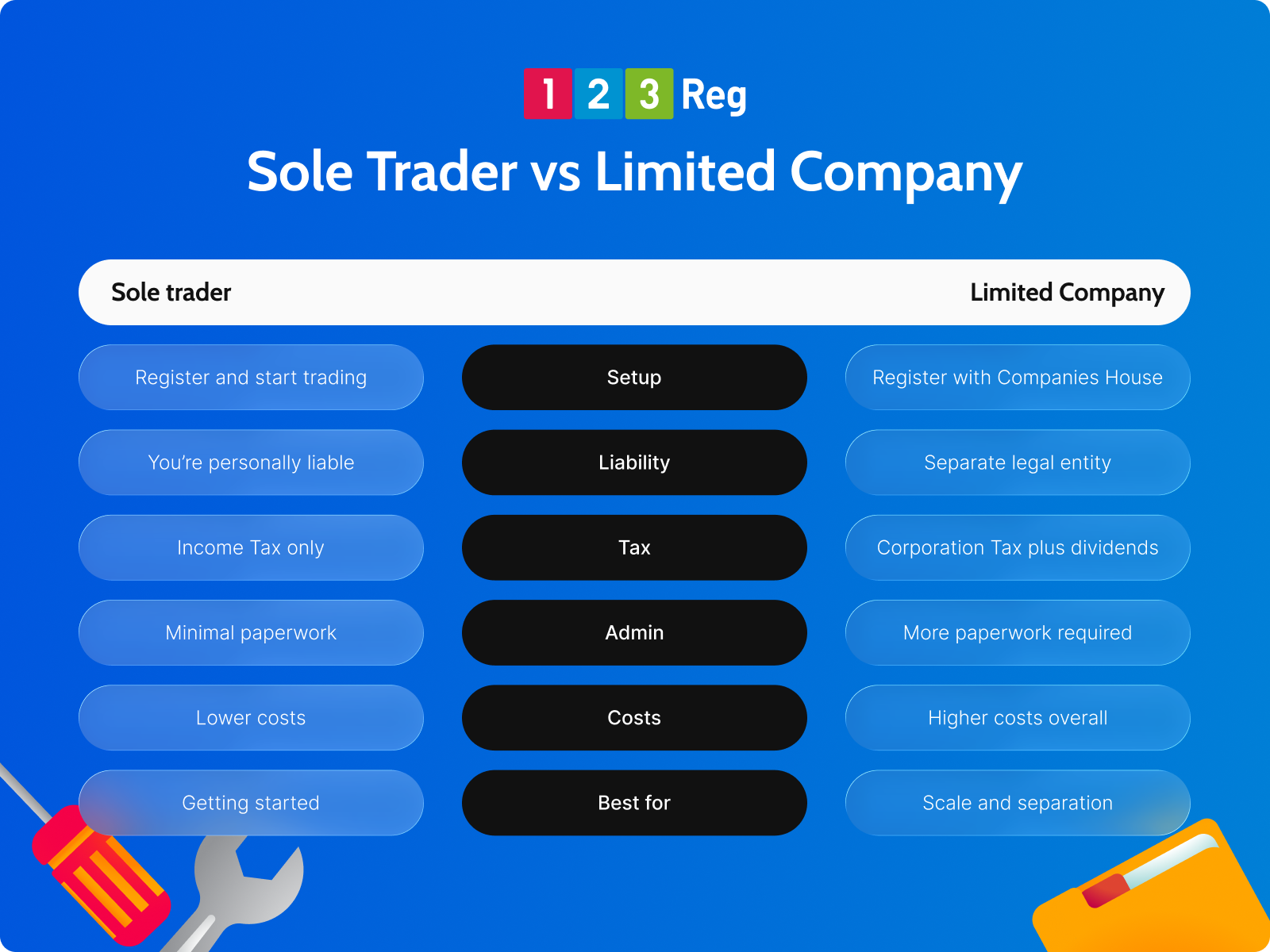

What’s the difference between a sole trader and a limited company?

There are several ways to structure a business in the UK, but for most people starting out, it comes down to two options: sole trader or limited company.

Sole trader

A sole trader is the simplest way to run a business. You and your business are legally the same entity. You keep all the profits, you make all the decisions, and you’re personally responsible for any debts or losses.

There’s no company to register, just you, trading under your own name or a chosen trading name. It’s the most common starting point for freelancers, contractors and small business owners. The admin is minimal, and you’re in complete control.

Limited company

A limited company is a separate legal entity from you as an individual. It has its own name, its own finances, and its own legal responsibilities. You can be both the director and the owner (called a shareholder), but the business exists independently of you.

With a limited company comes limited liability. If the business runs into debt or faces a legal claim, the company is responsible, not you personally. Your savings, property, and personal finances are protected.

It’s not a cast-iron guarantee against all risk, but it puts a clear legal wall between your business and your personal finances. That distinction matters more than it might seem when you’re just starting out.

How do I choose the right business structure?

There’s no single right answer here — the best structure for your business depends on where you’re at right now and where you’re hoping to go.

Most people work it out by weighing up a handful of practical factors rather than following a strict rule, so let’s take them one at a time.

☐ Your earnings are the obvious starting point

If you’re just starting out or earning modest amounts, a sole trader is usually the simpler and more practical choice. As your income grows, the tax and liability benefits of a limited company start to outweigh the extra admin.

☐ Risk is the next thing to consider

If your business involves contracts, significant expenses, or anything where things could go wrong financially, limited liability is worth serious consideration. For lower-risk work, a sole trader structure may be perfectly adequate.

☐ Admin is worth being honest about

A limited company means annual accounts, Corporation Tax returns, and Companies House filings. If you’re not planning to use an accountant, that’s a real time commitment.

☐ Who you’re selling to also play a part

For some businesses it rarely matters. For others, particularly those chasing larger contracts or working with corporate clients, being a limited company can carry more weight. It’s not always a deciding factor, but it’s worth thinking about.

☐ What you want to do online matters more than people realise. Some payment processors, affiliate programmes, and business platforms ask for a registered company name or VAT number when you sign up.

Certain business bank accounts are only available to limited companies. Even registering a domain name or setting up a business email address sits more naturally behind an official business name.

Sole Trader: Pros and cons

Being a sole trader is the most popular way to start a business in the UK, but it’s not without its drawbacks.

| ✓ Pros | ✗ Cons |

|---|---|

| It’s simple to set up. There’s no company to register. Just let HMRC know you’re trading and you’re good to go. The whole process takes minutes. | Your personal finances aren’t protected. Because you and your business are legally the same, any debts or legal claims against your business are also against you personally. |

| You keep full control. Every decision is yours. No board, no shareholders, no need to consult anyone else. | You pay Income Tax on all your profits. Everything the business makes is treated as your personal income and taxed accordingly. As your earnings grow, this becomes less and less efficient. |

| The admin is minimal. One Self Assessment tax return a year covers your tax obligations. That’s about as easy as it gets. | It can be harder to look the part. Some clients, particularly larger businesses, prefer to work with limited companies. It’s not a universal rule, but it can be a barrier when bidding for contracts. |

| You keep all the profits. Everything the business makes after tax is yours. No dividends, salary structures, or company accounts to think about. | Growth can be harder to fund. Banks and investors tend to look more favourably on limited companies. Getting a business loan or outside investment can be more difficult. |

| It’s easy to change later. If your business grows and a limited company starts to make more sense, switching is a well-trodden path. Starting as a sole trader doesn’t lock you in. | Your business name isn’t protected. A sole trader trading name isn’t registered anywhere officially. Anyone else can use it. |

Limited Company: Pros and cons

Going limited involves more admin and cost, but the benefits are significant once your business starts to grow.

| ✓ Pros | ✗ Cons |

|---|---|

| Your personal finances are protected. If the business hits serious trouble, your personal assets stay protected. The company is responsible for its own debts. | More admin involved. Annual accounts, a confirmation statement, Corporation Tax returns, and PAYE if you’re paying yourself a salary. |

| You can pay less tax as you grow. Limited companies pay Corporation Tax rather than Income Tax, and directors can take a mix of salary and dividends to keep their tax bill lower. | Your finances are on public record. Limited company accounts are filed with Companies House and visible to anyone. |

| It can open more doors. A limited company tends to be more appealing to bigger clients, lenders, and anyone you might want to bring into the business. | It costs more to run. Accountancy fees, Companies House filing fees, and potentially payroll software all add up. |

| Your business name is protected. Once registered with Companies House, your company name is legally yours. No one else can register the same name in the UK. | Less flexible with money. Taking money out of the business involves more structure — salary, dividends, expenses — rather than simply keeping what you earn. |

| Easier to bring people on board. A limited company makes it more straightforward to share ownership, raise investment, or scale up. | Closing it down takes effort. Winding up a limited company is a formal process. It’s not as simple as deciding to stop trading. |

Tax for sole traders and limited companies

Tax is one of the biggest practical differences between the two structures, and often the thing that tips people towards going limited as their income grows.

As a sole trader, your business profits are treated as personal income. You pay Income Tax on anything above your Personal Allowance (£12,570 in 2025/26), plus National Insurance contributions, and report everything through a Self Assessment tax return each year. It’s straightforward, but as your profits grow, you can end up paying more tax than you need to.

A limited company pays Corporation Tax on its profits, currently set at 19% for profits up to £50,000. As a director, you typically pay yourself a small salary within your Personal Allowance and top that up with dividends, which are taxed at a lower rate than income. Your company can also claim a wider range of allowable expenses. It involves more moving parts, but those moving parts can work in your favour.

For lower earnings, the difference is minimal and the extra admin probably isn’t worth it. But once your profits push past around £30,000 to £50,000 a year, the limited company structure generally means paying less.

Everyone’s situation is different, so it’s worth talking to an accountant before making the switch purely for tax reasons.

A note on tax figures

Tax thresholds and rates can change. The figures in this section are correct for 2025/26 but it’s always worth checking the latest rates on GOV.UK or speaking to a qualified accountant.

See also: I Sell Online. What Do I Need to Know About Making Tax Digital?

When should I change from sole trader to limited company?

There’s no single trigger point, but there are some clear signs it’s worth thinking about.

Your profits are consistently healthy and you’re paying a significant amount in Income Tax. You’re winning or chasing larger contracts where clients expect to work with a limited company. You want to protect your personal finances as the business takes on more risk. If several of those apply at once, it’s probably time to have a conversation with an accountant.

On earnings, there’s no official threshold, but £30,000 to £50,000 in annual profit is the range most often cited as the point where going limited starts to make financial sense. Below that, the tax savings often don’t outweigh the additional costs and admin.

If you’re still testing the waters with a side hustle, start as a sole trader. It’s low commitment and easy to change later. You just need to register with HMRC once your side income passes £1,000 a year under the trading allowance rules. When it becomes your main income and starts to grow, you can reassess.

Looking to become a dropshipper? Check out: How to Launch a Dropshipping Business in the UK

How do I change from sole trader to a limited company?

1: Register your limited company with Companies House

You can register online at Companies House for a fee of £50.

You’ll need to choose a company name, provide a registered address, and set out basic details about directors and shareholders. Most applications are approved within 24 hours.

2: Tell HMRC you’ve stopped trading as a sole trader

You’ll need to notify HMRC that you’re no longer trading as a sole trader and file a final Self Assessment return covering your last period of sole trader activity.

At the same time, you’ll register your new limited company for Corporation Tax, which needs to be done within three months of starting to trade.

3: Open a business bank account in your company name

A limited company must have its own separate bank account. This is a legal requirement, not just good practice. Your personal accounts and previous sole trader accounts can’t be used for company finances.

4: Transfer contracts, assets and agreements

Any existing contracts you hold as a sole trader will need to be novated (formally transferred) to your new company, with agreement from the other parties involved. The same applies to supplier agreements, leases, and any other formal arrangements. It’s worth getting legal advice if you have significant contracts in place.

5: Update your website and business email to reflect the change

Don’t overlook this step. Your website, email address, invoices, and any marketing materials should all reflect your new company name. If your domain name no longer matches your business, it’s worth registering a new one to keep things professional.

What happens when I switch from sole trader to limited company?

Transferring assets between structures is possible in both directions, but it’s rarely as simple as just moving things across.

Because a limited company is a separate legal entity, any assets transferred to it from your sole trader business are treated as a sale, even if no money changes hands. That can have tax implications, including Capital Gains Tax on certain assets.

Going the other way, from a limited company back to sole trader, the same principle applies: the company disposing of an asset is treated as selling it, which can trigger Corporation Tax on any gain.

In either case, an accountant’s advice before you start moving anything is strongly recommended.

What other business structures are there?

Sole trader and limited company cover the majority of small businesses, but they’re not the only options.

A partnership is essentially a sole trader arrangement with two or more people. Each partner shares responsibility for the business, including its debts. A Limited Liability Partnership (LLP) works similarly but gives partners the same liability protection as a limited company. Partnerships are common among professionals like solicitors or accountants.

A social enterprise is a business that trades with a social, environmental or community purpose at its heart. Profits are typically reinvested into that mission rather than paid out to owners.

They can be structured in several ways, including as a limited company or a Community Interest Company (CIC).

If your business does indeed have a social mission, The King’s Trust and gov.uk both offer help on getting started.

If you’re after ideas, check out: 40 Easy Online Business Ideas You Can Start Today

Do I need a website for a business?

Some businesses start out purely through social media or third-party marketplaces, but a website gives you something no social profile can: a branded home on the internet that’s entirely yours.

Your domain name is part of that brand. With over 400 endings to choose from — .co.uk, .shop, .studio, .agency and more — you can find something that tells people exactly what you do before they’ve even clicked.

Everything you need to get online

123 Reg’s Website Builder and Managed WordPress Hosting plans both include a free domain name and professional email address. Get your business online with everything matching from day one.

For more, check out: How To Get a Free Domain Name and What are the Benefits of a Professional Email Address?

Where can I get free business advice and guidance?

You don’t have to figure all of this out on your own. These are the most reliable places to go for free, authoritative guidance.

GOV.UK: The official government resource for registering a business, understanding your tax obligations, and everything in between. Clear, straightforward, and regularly updated.

business.gov.uk: A practical hub for small business owners covering finance, legal basics, hiring, and more.

Companies House: Where you register a limited company, file accounts, and manage your company records. Their guides for new directors are worth a read.

HMRC: For everything tax-related, from Self Assessment to Corporation Tax to VAT registration.

The King’s Trust: If you’re aged 18 to 30 and starting your first business, the King’s Trust (formerly the Prince’s Trust) offers free mentoring, funding support and practical guidance to help you get off the ground.

One last thing before you go

Whichever structure you choose, getting your business online with a professional website and a matching email address is one of the best first moves you can make. 123 Reg’s Website Builder and Managed WordPress Hosting plans include a free domain and professional email. Everything you need to get started, all in one place!

FAQ

Can a sole trader become a limited company and then switch back?

Yes, technically. Going from sole trader to limited company is straightforward. Going back the other way means formally closing the limited company, which involves a process with Companies House. It’s doable, but not something to do on a whim.

Can two people run a business as sole traders?

Not as a single business. If two people are running a business together, it’s a partnership by definition. Each person can be a sole trader in their own right, but only for their own separate business activities.

Do I need an accountant to set up a limited company?

No, you can register directly with Companies House yourself. That said, an accountant is worth the cost once you’re up and running, particularly to help with Corporation Tax returns and making sure you’re paying yourself in the most tax-efficient way.

Can I use my home address to register a limited company?

Yes. Your registered address just needs to be in the UK and able to receive official correspondence. Bear in mind it will be publicly visible on the Companies House register.

What’s the difference between a business name and a company name?

A business name (or trading name) is what you call your business day to day. A company name is the legally registered name on Companies House. They can be the same, or a company can trade under a different name to its registered one.

Do I need to register for VAT?

You must register for VAT once your taxable turnover exceeds £90,000 in a 12-month period. You can also register voluntarily before that, which can be beneficial if your customers are VAT-registered businesses themselves.

See also: How to Find VAT Number by Company Name

Can I run more than one business under one limited company?

Yes. A limited company can trade under multiple trading names, covering different business activities. Whether that’s the right approach depends on your situation, and it’s worth discussing with an accountant.